Tesla's earnings visualized

Tesla's earnings visualized

And a short analysis of the earnings.

Hi dear reader

Tonight, Tesla (TSLA) announced its Q1 2023 earnings. As usual for Tesla, bulls and bears are already rolling over Wall Street to claim they are right. With this income statement visualization, you have the data to form your own opinion. I hope you enjoy it.

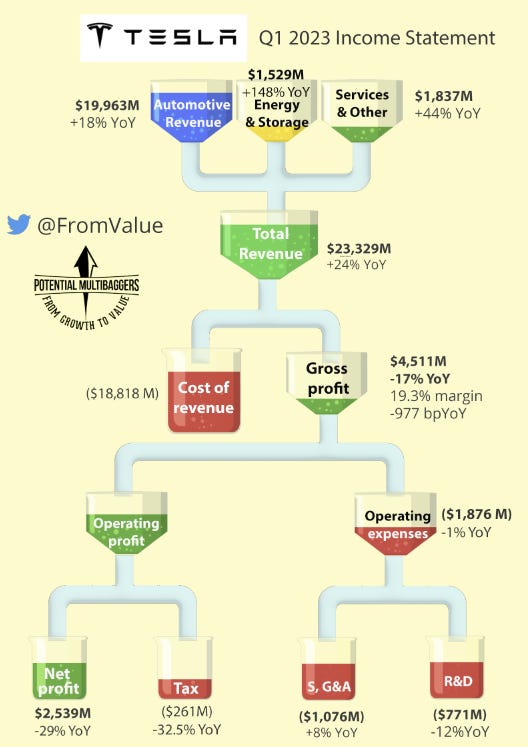

Tesla had EPS of $0.85, in line with expectations. For revenue, it missed the consensus by $60 million, a rounding error of 0.25% on total revenue of 23.33 billion.

What stands out here are the margins, which dropped a lot. That was caused by a one-time warranty cost and lower margins at the new gigafactories in Austin and Berlin. For the rest of the year, its expected margins will improve again from efficiencies in the new production facilities and lower commodity prices. Management said mid-20s margins should be expected again.

Free cash flow was impacted by the same things, by paying off debt and the investments in the new production facilities. But Tesla still generated $440 million in free cash flow.

The company still expects to exceed its 50% production growth for this year and it projects that the Cybertruck will be produced in Q3 of this year.

There may be much fuss, but to me, as a long-term investor, I don’t see too many flaws. Yes, margins are lower, but the explanation seems sensible. Energy and storage, which is one of the reasons I have a position in Tesla, are growing like weeds and will continue to do so for many years.

In the meantime, keep growing!

If you don’t want to miss similar short updates after earnings, feel free to subscribe.

Thanks for the update!