Roku: Was That 24% Drop Warranted?

Roku: Was That 24% Drop Warranted?

Summary

On Thursday after the market, Roku reported its Q4 2023 earnings.

The stock dropped like a rock attached to a brick on Friday, down 24%.

Were the earnings that bad or was this drop unwarranted?

I tell you what I will do with Roku in my portfolio.

Hi friends

Last week was an extremely busy week for me. I published 9 articles on Potential Multibaggers, my Seeking Alpha paid service. This article is one of them. If you want to read everything, you can try out Potential Multibaggers for free for two weeks and get a 20% discount. You can read everything and decide to quit during the free trial with just a few clicks.

Click here for your FREE TRIAL and 20% DISCOUNT.

On Thursday, after the market bell ended the trading day, Roku (ROKU) reported its Q4 2023 earnings and on Friday, the stock dropped like a rock attached to a brick.

In this article, I examine why and what I will do with my Roku position. If you don’t want to miss these free articles, don’t forget to subscribe to this free service, Multibagger Nuggets.

Before we go to the numbers, I want to show you this: the implied move; in other words, how much can you expect the stock to move? You just don't know which direction…

As you can see, the implied move for Roku was 15%.

This seems to be quite correct for the after-market move. The next day, some extra loss was added. I think we should always consider that these short-term movements often have to do with trading and not by a careful analysis of the numbers.

The Numbers

Q4

Revenue came in at $984.4M, up 13.5% year-over-year and beating the expectations by $17.29M or 1.8%.

The GAAP EPS was -$0.55, meeting the consensus.

Active accounts 80.0 million, up 10.0 million or 14.3% from 2022.

Streaming Hours 106.0 billion, up 18.6 billion hours or 21.3% year-over-year

Average Revenue Per User ('ARPU') was $39.92 on a trailing 12-month basis, down 4% year-over-year.

Some commenters cited the lower ARPU as a reason for the big drop and the "negative evolution in ARPU." See this excerpt of Seeking Alpha’s summary of the analysts’ takes for example:

And this is also from Seeking Alpha:

That sounds informed and can be proven with a graph.

But you should know that analysts have a severe case of explanation compulsion. They feel they have to come up with an explanation, even if they don't understand it. There must be an explanation, right? Especially if the stock drops by 15%

But in this case, they ignore that the ARPU has been trending down for a while, since Q4 2022, as you can see. In its shareholder letter, which is always really good by the way, management also always explains this. The somewhat lower ARPU reflects

an increasing share of Active Accounts in international markets where we are currently focused on growing scale and engagement.

This perfectly makes sense. Everybody knows that the US has the highest-paid ad market in the world and expanding internationally will always lower the ARPU. If there's one thing I'm a bit surprised by, it's the fact that ARPU doesn't drop faster. This shows an underlying strength in the US that partly offsets the lower ARPU of the international expansion.

As a reference, this is Pinterest's (PINS) ARPU, split up between US and international.

As you see, there's a massive difference between the US and the rest of the world. You can also see how much higher Roku's ARPU is compared to that of Pinterest, which is because the CPM (cost per mille, what it costs for an ad for a thousand views) is much higher for CTV than for the internet and in-app ads. So, the somewhat lower ARPU is no reason at all for me to worry. If you hear this, it's either someone who doesn't know the company well or has an explanation compulsion that makes no sense.

Full-year 2023

A fast overview of the key metrics:

Total net revenue was $3.5 billion, up 11% year over year year-over-year

Platform revenue was $3.0 billion, up 10% YoY

Gross profit was $1.5 billion, up 6% YoY

Active Accounts were 80.0 million, a net increase of 10.0 million from 2022

Streaming Hours were 106.0 billion, up 18.6 billion hours YoY

Average Revenue Per User (ARPU) was $39.92 (trailing 12-month basis), down 4% YoY

Achieved positive Adjusted EBITDA and Free Cash Flow for full year 2023, ahead of schedule

Guidance

Roku beat the estimates, but its stock still cratered by 24%. Often, that has to do with bad guidance, but that was not the case for Roku.

The company expects Q1 revenue of $850M, better than the $835M consensus, gross profit of about $370M and break-even adjusted EBITDA.

My point of view

I want to remind you of Roku's business model, where devices are a way to get to platform revenue. The devices, like the sticks, the TVs, the smart home systems, the soundbars, and remote controls, are a way to get Roku's operating system into people's houses. Roku interjects ads into the content or makes a bit of money from subscriptions.

More concrete. If you subscribe to Netflix or Disney+ through Roku, Roku gets a small percentage of the subscription, 1% to 5%, usually. And if a CTV channel is ad-driven, and it has an ad block of 3 minutes, Roku will add an ad of 30 seconds or so, of which it gets a big part of the revenue, depending on the contract with the streamer and the formula they chose. So, they can lose money on the devices without any problem. Over time, they make it back and then some on the platform side of the business.

You can also see that in this overview of the company's numbers.

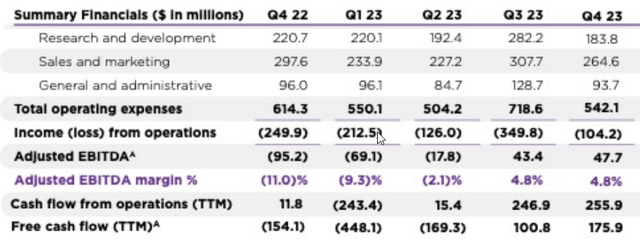

The overview continues and I want to give it here, as it gives insights about how much the picture improved for Roku over the last year.

As you see, the company generated $175.9 million in free cash flow in the fourth quarter of 2023, up from a loss of $448.1 million in Q1 of 2023 and a loss of $154.1 million in Q4 2022.

So, yes, on paper, this is a "loss-making company," but there's always a massive difference between a company that has free cash flow and a company that doesn't. The main difference between GAAP losses and positive free cash flow is usually SBC or stock-based compensation. For Roku, this was $92 million in the fourth quarter, 9.3% of revenue, which is relatively low for tech. On top of that, SBC is down 12.4% year-over-year.

There is also depreciation and amortization. In the “content industry”, the amortization of content is a crucial element. As anyone who follows Netflix (NFLX) knows, this is somewhat misleading. You have to amortize the expenses of content fully in the first year. So, if you paid $10M for content in 2023, you have to amortize that full amount in 2023, while after years, that content can still generate money through ads if someone watches a movie or a series bought or produced a few years before.

The last difference between positive FCF and negative GAAP net income was a one-time charge of $42 million related to lease impairments and workforce reductions.

As an investor, you don't have to worry at all about Roku's financial situation. The company is free cash flow positive and on top of that, it has $2 billion in cash and equivalents and no debt. Add the $816 million in receivables minus $386 million in payables and you can even add another $430 million. In other words, Roku's financial situation is solid as a rock.

I want to highlight the number of active accounts and the number of hours streamed.

I highlight them because these are, in a way, very clean numbers. They exclude the cyclicality of the ad market and show how Roku's operating system is distributed across different channels: sticks, the company's own devices, and licensed operating system partners on the one hand (for active accounts) and how popular the system is among customers (number of hours streamed).

21% growth in hours streamed is in stark contrast with the sharp decline in hours on traditional TV in the US, down 16%, year-over-year, according to Nielsen. It's important to notice that Roku also grew significantly faster than the overall streaming industry.

The Roku Channel, Roku's own channel, grew even much more, with 63% more hours streamed compared to the same quarter in 2022. This is important for sponsorships as well. From the shareholder letter:

In Q4, we attracted strong advertiser interest with a viewer experience created specifically for the holidays. The experience featured thematic licensed programming, pop-up holiday FAST channels, and a lineup of new Roku Originals including How to Fall in Love by the Holidays sponsored by Walmart, The Holiday Shift sponsored by Kohl’s, and The Great American Baking Show: Celebrity Holiday sponsored by State Farm.

Streaming hours per active account per day grew to 4.1 hours in Q4 2023, up from 3.8 hours in Q4 2022 and 3.6 hours in Q4 2021. On traditional TV, this is 7.5 hours per day, showing there is still room for growth for Roku.

Streaming hours from Roku's home screen more than doubled year-over-year. That's great, as Roku monetizes its home screen as well. It also upgraded the search function and streaming from search increased by 50% year-over-year.

Don't forget that Roku has introduced shoppable ads. While it's still very early for those, they look very promising, and engagement numbers will be very important for the success of shoppable ads. The numbers show that the click-through rate from shoppable ads is 3 to 5 times higher than on the internet.

This is an example of Coca-Cola partnering with DoorDash.

Revenue growth will be much lumpier, as it is influenced by the demand for ads, the price of ads, the number of new subscriptions for paid channels and many other parameters.

In other words, over the long term, the number of active accounts and hours streamed should show you the long-term revenue growth and eventual profits. It would be logical that revenue growth grows in-line with hours streamed, as the more hours streamed, the more ads Roku can interject. But it's not that simple, as the hours streamed also include paid subscriptions, where there are no ads. If you ask my guess, I would say that the average (!) revenue growth over the long term would be somewhere in between the two numbers, hours streamed and the number of active accounts. Of course, ARPU also plays a role in the equation and we should expect that to slide slowly as there is more international expansion, so that might tip the balance a bit more to active accounts than to hours streamed.

Roku is totally not optimized for monetization yet. It's still in land-grab mode and to me, that's absolutely the right choice for now. There is still a lot of land to grab. Roku became the most dominant player in the US by using this strategy, beating giants like Amazon (AMZN) and Google (GOOG) (GOOGL). If it wants to accomplish the same thing internationally, it will have to continue this strategy for several more years. In a short time, Roku became the dominant player in Canada and Mexico as well, and it's becoming more important in Brazil, Chile and other countries in Latin America. Usually, this goes through partnerships with OEMs like Sharp, JVC, RCA, TCL, Philips and many more. Roku also has its own branded TVs.

There is another very important growth driver for Roku in the medium- to long term. From the shareholder letter:

In 2023, U.S. adults aged 18-49 spent more than 60% of their TV time on streaming, while advertisers spent just 29% of their TV budgets on streaming.

This will go up over time. Targeted ads are superior in many ways compared to traditional TV. The name already suggests it: they are much more targeted and also much more measurable, showing advertisers how much return they get on their ad investment.

Insights from the earnings call

Founder and CEO Andrew Wood announced Roku's strategic goal for 2024. In 2023, this was more focused on internal metrics like efficiency, cost reductions and operational improvements. This is what Roku will focus on in 2024:

This year, we will be redirecting much of our attention to platform growth and innovation, where I see lots of opportunity. A core strategy for us is to take better advantage of our position as the programmer of the home screen for our 80 million active accounts globally. We use this to grow ad reach, which correlates to add revenue, as well as to grow our streaming service distribution activities.

According to Wood, Roku is positioned very well for the two strongest trends in TV streaming:

I see two trends that are particularly important for us. One is the enormous volume of streaming content. As I just mentioned, helping our viewers easily navigate and find what they want to watch is a big opportunity for Roku.

Second, the industry has increased its focus, now more than ever, on building thriving and sustainable businesses. This means more ad supportive streaming service tiers, which will further accelerate the overall shift of ad dollars from traditional TV to streaming. Roku has the tools and expertise to help streaming services grow engagement, which is critical in an ad supported environment.

The company said that advertising is growing again after a tough 2022 and 2023 but not all sectors are recovering at the same speed. The financial sector and M&E are especially lagging. M&E stands for media and entertainment and it has always been a significant sector for Roku. It's also intuitive that companies like Netflix, Disney, or others would advertise on Roku's home screen or through ads to capture the viewer's attention. Anthony Wood on the M&E industry:

They spent a lot of money on M&E in the go-go years of the COVID-19 pandemic. Now that they're retrenching and focusing on a sustainable business, that spending has normalized, it's normalized down a little bit. But it's going to continue to pick back up, and over time, it will be a growth business for us.

One more thing before we go to the conclusion: Charlie Collier made a great impression again on the conference call. I read a comment somewhere that it would be a good idea to send Charlie to CNBC instead of Anthony Wood. I have huge respect for the founder CEO, but Charlie has more natural charisma and I think this would benefit Roku indeed.

Conclusion

When you see a stock drop so much, there must be something you missed, right? It's impossible a stock just drops because of nothing, is it?

Well, I looked at all the numbers, I listened to management and read the earnings transcript, just in case I missed something and I don't see it. To me, the 25% drop is the result of traders and weak hands that threw in the towel.

I'm not selling my Roku position, therefore. I'll even add a tiny bit for the first time in a while.

I want to make it clear it could take years before the market understands and appreciates that Roku is just grabbing as much land as possible in this market now and it's a powerful player, much more powerful than the market thinks. It reaches more than half of the households with broadband in the US, it's the number one player in Canada and Mexico and getting stronger in other markets, especially Brazil, where it's a fast grower.

It will probably only be when Roku starts focusing on monetization more that the market will understand this better. I'm willing to wait for years. I see no fundamental flaws in these earnings. Yes, the company is dependable on the cyclical ad market, but that's inherent to the business. These cycles come and go. It's important to separate the stock price action from the fundamentals. I quickly saw comments like: "Awful earnings from Roku." To me, these are only inspired by the stock price move. I saw strong earnings and strong guidance.

To rate the earnings, this is how I see them.

That is good if you want to see it translated into language. Not blowing all expectations out of the water (awesome) but definitely more than just "okay."

One more thing about the rumors that Walmart will buy Vizio, I also heard the rumor that they would throw out the operating system and replace it with Roku’s. Don’t forget that Walmart’s Onn TV brand also has Roku. I don’t know how reliable both rumors are. I’ll evaluate that news once it’s certain, but even if Walmart buys Vizio and uses its OS, I don’t see it as a death blow at all for Roku.

In the meantime, keep growing!

I haven't seen your article in years (former subscriber on seeking alpha), and it's funny how this Roku one sounds so familiar, still the same stuff years later. People buying to hold stocks for decades but then changing their minds after one earnings reaction hehehe. Do not miss those days, nor the noise.