Preparing The Trade Desk's Earnings report

Preparing The Trade Desk's Earnings report

Looking back to look forward

Hi friends

On Wednesday, The Trade Desk reports its Q1 2023 earnings. This is an analysis of the previous earnings. I think it will help rereading this for a few reasons:

What to look for in the upcoming earnings?

Does management follow up on certain themes?

The trends in advertising right now

Tracking Jeff Green’s bold predictions

Getting into the right mindset.

Checking the valuation

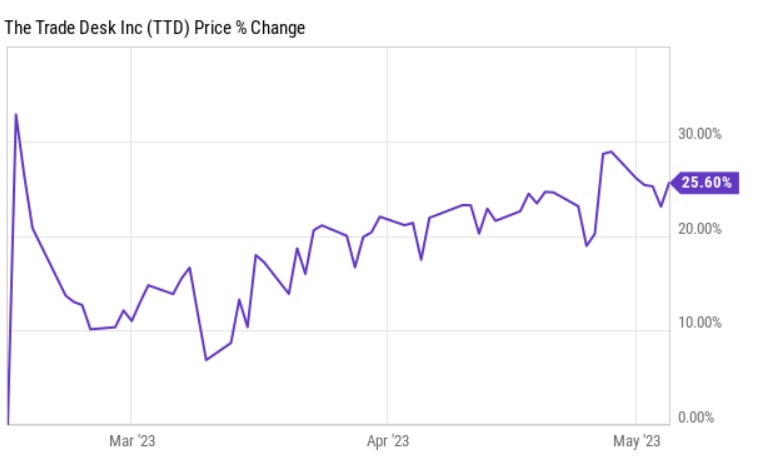

Just to remind you, the Trade Desk’s stock shot up 30% after the previous earnings. As is usual then, it came back to earth a bit, but it’s still up 25.6% right now compared with before the earnings.

Don’t forget that The Trade Desk has also been down 25% after earnings before, so big moves are always possible. To be honest, I don’t care too much about the immediate price action. If the stock goes up, great. If the stock drops, great as well; I can add more shares for the same money then. My goal is not to be in the green now, but in 20 years+.

I started a portfolio for the subscribers of Potential Multibaggers near the top of the market, in July 2021, to show how I build a portfolio. My position in The Trade Desk is in green there, despite the general market drop and the fact that The Trade Desk is still down considerably when compared to then.

How can I be up when the stock is down? Simply by dollar-cost averaging. I have written about that before on this blog.

Now, let’s go to the Q4 2022 earnings, to prepare for the upcoming earnings. This is what you can expect in the rest of this article.

We look in more detail at what The Trade Desk exactly does and why it's different from the walled gardens, Meta Platforms and Google.

The numbers show that The Trade Desk takes even more market share in this tough economic time than in a bull market.

Jeff Green again gave valuable insights into ad tech and made some bold predictions.

We look at the valuation of the stock.

I have a strong sense of hesitant optimism about what 2023 holds for our industry.

Jeff Green, founder and CEO of The Trade Desk on the Q4 earnings call

The company also announced a share buyback program of $700 million.

Before we dive into the earnings, let's look again shortly at what The Trade Desk does. If you don’t know exactly, this is a good introduction. For people who already know, I will try to do it a bit differently than usual, so it's not too dull. Of course, you can also skip this part and immediately go to the earnings if you already know very well what the company does.

What The Trade Desk does

Just to remind you shortly about what The Trade Desk does, this slide from the Q4 2022 earnings call slide deck can help you.

In short, The Trade Desk is similar to a stock broker's platform but then for ads. As it says:

The yellow tagline 'Even media that isn't digital will be transacted digitally using the internet' refers to, for example, in-store ads that are transacted on The Trade Desk's platform. If you want your article highlighted through a display in Walmart or Home Depot, that's possible on The Trade Desk. What makes The Trade Desk special is that it is a neutral platform. Brands can trust The Trade Desk with their data. For brands, this is very important as they have their customers' trust.

The Trade Desk measures all of its ads and provides those insights to its customers. As The Trade Desk is a neutral party, you can be sure those measurements are correct, just like the information from your stock broker is (almost always) correct.

During the conference call, CEO and founder Jeff Green emphasized why The Trade Desk will continue to take market share from walled gardens like Meta and Google. I highlighted the most essential parts of the quote.

If you know that the walled gardens are Meta Platforms and Alphabet's Google, I think the title of one of my previous articles on The Trade Desk was correct.

The opportunity for The Trade Desk remains big. The company rightfully emphasizes that it operates in a vast market.

For context, The Trade Desk had $7.9 billion in transactions on its platform, so it's only scratching the surface. You can also see that in the revenue split between the US and international.

While 67% of ad spending is done outside North America, The Trade Desk only generates about 10% of its revenue outside North America. The company has already set up offices in light blue countries, but it takes time to build relations, and most offices are still relatively new.

The Earnings Numbers

The Trade Desk’s Q4 2022 revenues grew 24% to $491M, a slight miss of $1.07 million compared to expectations. That's just 0.2%, so that's a rounding error and to me, revenue was in line with the expectations. Non-GAAP EPS came in at $0.38, beating the consensus by $0.02. This is a schematic overview of the earnings I have made.

For the full year 2022, The Trade Desk's revenue jumped by 32% to $ 1.58 billion. If you see the historical revenue growth, it's impressive.

(From the Q4 2022 earnings slides)

The results were not exceptionally outstanding for a company like The Trade Desk. The market was just relieved, I think, that The Trade Desk could chalk 24% revenue growth in such a challenging environment for ad-based companies.

Don't forget that even Google's ad revenue was down 4% year-over-year in Q4 and Meta's revenue went down for the third consecutive quarter. And those are among the strongest companies out there. If you look a bit deeper into ad-driven businesses, you see that Digital Turbine's Q4 revenue decreased by a whopping 25% year-over-year. Criteo, often seen as a direct competitor to The Trade Desk, saw its revenue decline by 13.6% in the fourth quarter.

So, bringing in the revenue in line with the expectations and growing 24% in such a difficult context, all organically, is good execution. Many short sellers were betting on The Trade Desk missing the consensus, like others in the ad industry, and meeting (for revenue) and beating (on EPS) caused a short squeeze. Jeff Green also mentioned The Trade Desk's strength in the press release:

In an unpredictable macro environment, our growing relationships with agencies and brands is testament to the value of the open Internet over the limitations of walled gardens.

The fact that for the 9th year in a row, The Trade Desk could keep customer retention above 95% both for the year and the quarter was also impressive in this environment.

We saw The Trade Desk guide Q1 revenue of 'at least' $363 million, in line with the consensus (although analysts don't work with at least), and EBITDA of $78 million. In the meantime, the analyst consensus has gone up slightly to $364.5 million. That means revenue is expected to grow at 15.5% in Q1, but again, in this environment, that's not bad at all. Although The Trade Desk does much better than the other players in ad tech, it also feels the macroeconomic headwinds. The company will continue investing and hiring, but will only add half of the number of people of 2022.

The Trade Desk saw very few cancelations, but there was a delay in the order execution in Q4. CFO Blake Grayson said that if you exclude the Q4 2022 elections spending, the quarter-over-quarter growth quarter-over-quarter (the results from Q4 and guidance of Q1) is even slightly better than usual, another sign of strength.

The Trade Desk's Board approved a buyback program for up to $700M, meant to compensate for the impact of dilution from stock-based compensation.

Usually, I'm not that fond of buybacks for growth companies, but I understand it in this case. After all, The Trade Desk has been GAAP (!) profitable since 2013; it has cash and short-term investments of almost $1.5 billion, invests more than enough in innovation and growth and generates more and more money each quarter.

Insights from the conference call

Conference calls with Jeff Green, founder and CEO of The Trade Desk, are always great. Unlike many other CEOs, you will not get bored by the usual business formulas of people congratulating themselves. You'll hear a passionate man eager to explain as much about the industry as possible to everyone. It’s pure passion.

By the way, if you haven't heard this excellent podcast episode yet, in which Jeff Green talks with Patrick O'Shaughnessy in Invest Like The Best, I would highly recommend it.

Green highlighted that CTV remained the most significant driver for revenue growth.

CTV continued to be our strongest growth driver as more content owners from around the world are moving beyond ad-free subscription models and offering ad-supported options for viewers.

Green even called CTV "the kingpin for the open Internet." There are no walled gardens in CTV like Meta and Google. And as more and more TV ad money goes to programmatic advertising, this is very lucrative for The Trade Desk. Jeff Green again:

Not only is the shift from linear to CTV driving significant growth in digital spend as advertisers shift dollars from linear TV to connected TV, but more spend is happening outside the walled gardens as advertisers shift spend from user-generated content to premium streaming content.

Green says that the shift will not be linear.

It won’t be a long gradual shift to CTV. It will be an acceleration and then a full long shift.

A few years ago, The Trade Desk developed UID 2.0, which it later gave away as an open-source product. It's an essential tool for winning against the walled gardens. Jeff Green explains again what it is and why The Trade Desk developed UID 2.0.

A few years ago, we created in collaboration with other open Internet companies an identity currency for the open Internet based on either an e-mail address or a phone number. UID2 is anchored on those two consumer data points so that consumers can own and manage their identity around the Internet rather than managing privacy settings for each device or ecosystem like Apple or Google.

Our goal was to create a personalization technology that was more privacy safe than cookies and better at empowering consumers than any alternative in the market.

And UID 2.0 is a great success. I highlight the most important parts of this quote again.

This was misunderstood by many investors, who thought, indeed, The Trade Desk would have to convince millions of content owners. While some big wins were announced, by integrating UID 2.0 into the internet's infrastructure, content owners started using the standard almost automatically, mainly because they knew cookies would be phased out.

By upgrading the data infrastructure of the Internet, there is now a significant mathematical incentive for every reputable player involved in digital advertising to lean in to UID2.

And the results for brands are much better with UID2.0. Jeff Green again:

Leading advertisers running campaigns on Disney, leveraging UID2 have been 12x more effective in reaching their targeted audience than without UID2. That’s astonishing progress. And it’s just the beginning.

It's always hard summarizing conference calls from The Trade Desk, as Jeff Green says so many interesting things. Sometimes, these included his vision for the future and if he sees that as fit, he doesn't shy away from bold predictions.

I have followed The Trade Desk for over five years, and each of his predictions has become a reality. He said Apple would have to postpone IDFA changes and it did. He predicted Google would have to postpone the abolition of cookies and it did so twice. He predicted that CTV would become huge and break walled gardens and that’s happening. And those are just three examples from the top of my head. There are many more.

To be honest, I was skeptical about some of these predictions, as Green predicted things outside of The Trade Desk's power, but these predictions (and many more) proved to become a reality repeatedly. If visionary means predicting the future, I only know a few CEOs that have done that as consistently and accurately as Green.

Regarding CTV as the hammer breaking down walled gardens brick by brick, Green predicts 2023 will be a pivotal year.

I also believe that 2023 will be the year that every theme in TV changes.

Green refers to the upfront market. It was invented in 1962, together with the cassette tape. The upfront market means brands/advertising and TV executives get together and make a deal about advertising spending in the upcoming year. The upfront market has almost not changed since it was started and that has to change fast, according to Green.

The opposite of the upfront market is the scatter market, where brands decide last minute (as it were) to add to their advertisement campaigns. This part of the advertising market is fragile right now and one of the main reasons Roku is struggling. So, that's not what Jeff Green wants to replace the upfront market by. He explains how he sees the changes:

The market needs an upfront that is always on, but also leverages data so that content owners sell fewer, more relevant ads at higher CPMs and advertisers get more efficacy.

What Green means by 'an upfront that is always on' is that you shouldn't commit your ad dollars for the upcoming year, but you should be able to commit them for the next day if you want that. The effectiveness should be constantly measured and that should drive more actions. He compared it to commodity markets.

If you know your campaign's ROI, you can add more money or alter your campaign a bit to get the ROI higher. Through its partnerships with Walmart, Home Depot, Albertsons, and in total 80% of the leading retailers in the US, The Trade Desk can provide these insights locally or in big areas.

Everyone wins in this situation:

Brands know their ads reach targeted audiences. Even if these cost more, they are converting much better and worth the extra price tag. They can also adapt their campaigns and spend through almost real-time insights.

Consumers see fewer ads and those they see are much more relevant to them.

The Trade Desk gets more revenue.

While this is probably an inevitable situation because of the added value to all parties, this will not change in one year or so.

To adjust for high CPMs in CTV today, advertisers are asking us for a new forward market where they can leverage data on an everyday always-on basis. Advertisers have to make their ads more effective to justify higher ad prices. It takes a long time to unwind the culture of multibillion-dollar commitment signed during a few days each spring and bring the process into today’s digital environment.

Jeff Green announced an event in March before the upfront market season, which usually starts in May and lasts a few weeks. The Trade Desk wants to show everyone that there is a better alternative.

Important Shifts In The Ad Market

Jeff Green sees two fundamental shifts in the ad market.

The first is what he calls the shift from impressions to value. As advertisers can access more data for their campaigns across multiple channels, they will start prioritizing value over just the price. While they will still consider the cost of buying ad space, they will focus more on whether the ads delivered the desired outcome for the price paid. Green even goes as far as calling this correcting a historical mistake. Impressions should never have been a measuring stick; conversion should be.

Until now, inventory was low in CTV, because most streaming was subscription-based. That meant high CPIs (cost per mille, so how much 1,000 impressions cost an advertiser). With Netflix and others adding an ad-based model, the low inventory can no longer be based on scarcity. That's why content creators are more willing to add measurability, often through UID 2.0. That enhances brand value, and therefore CPIs don't have to drop. Think of that example with Disney, where they saw 12 times more effectiveness. With the additional value, brands are happy to pay these higher CPIs because more targeted ads and more flexibility in terms of spending gives them a better ROI.

We let Green explain the second shift, which is a consequence of the first one:

in the pursuit of value, advertisers decisioning will shift from inventory to audience. Instead of focusing on buying a certain show or a certain piece of inventory, advertisers will put much more priority on audience precision regardless of channel, because data enables them to do that. This is especially important as the industry moves from a once-a-year upfront to an always-on forward market.

The words 'regardless of the channel' are essential because The Trade Desk can offer any channel an advertiser wants.

Jeff Green always talks about the value exchange of the internet: you give something, and then you get something back. In this case, you get free content. The only thing I ask is to subscribe to Multibagger Nuggest. There’s a paid version for just $80 per year or $8 monthly. Or you can read these articles for free for two weeks. Make sure you don’t miss them.

Two Jeff Green Predictions

Green added two predictions again. I'm pretty confident he will be proven right, looking at his track record.

This is the first one.

I also predict that more walled gardens will begin to take down some of their barriers. They will see that incremental demand and higher CPMs that companies like The Trade Desk can generate with a focus on advertiser goals, data and the open Internet.

In the Q&A section, Green even went further and predicted that change would already show up in 2023.

I do believe you will see announcements in 2023 suggesting more and more walls coming down.

The second one is about the DOJ case against Google.

We have been winning for years in an unfair market with some systemic obstructions working against us. Imagine what we can do as the market becomes more fair which we predict it will one way or another.

According to Green, this time, it's different when it comes to the case against Google. (Just like Green, I refer to Google, not Alphabet, because the ad business is entirely in the Google branch).

Valuation

If you have a great company in a massive total addressable market, growing its revenue fast and expected to do that for a very long time, you can't expect the stock to be cheap. And judging a growth stock on a PE never makes sense, although I still see many comments suggesting to do that.

Even price to free cash flow or forward PE won't tell you that much, as they are often too volatile. This is the last year, for example.

A better alternative for valuation in growth investing is The Rule Of 40. It adds the percentage of revenue growth to the profitability margin. If the number is above 40, you have quality growth. There is some discussion about what kind of profitability to use. Should you take free cash flow or EBITDA? Usually, FCF is used.

Many value investors don’t get the high valuations of growth stocks, but there is an explanation. You can see in this graph that the valuation indeed depends on the Rule of 40. The higher the revenue growth and FCF margin, the higher the valuation.

An advantage about the Rule Of 40 is that you can adapt it to your own wants. Do you want at least 25% revenue growth? Do you want at least 15% FCF margins? You can set that as a precondition and weed out companies that don't meet your standards.

Of course, the best companies can use both engines, revenue growth and FCF. And The Trade Desk is such a company. Whether you choose EBITDA or FCF for The Trade Desk, it doesn't matter. If you add revenue growth, you get to a score of over 50 and even 60. Very impressive and even more in this environment with macroeconomic headwinds.

Conclusion

The Trade Desk keeps impressively outperforming its industry. It already did that during a bull market, but it proved in Q4 2022 that it could also do that in tough economic times. Jeff Green has always said advertisers would come even faster to The Trade Desk in difficult times, as they have to accomplish results with lower budgets. That's precisely what's happening now. It's very confidence-inspiring to see that.

The Trade Desk is a core holding since I picked The Trade Desk as a Potential Multibagger at (a split-adjusted) $19.5, and it will remain a big position for me as long as the company keeps executing at this high level.

If you have come this far and haven’t subscribed to Multibagger Nuggets yet, don’t hesitate. It’s free.

In the meantime, keep growing!