Google's earnings

Google's earnings

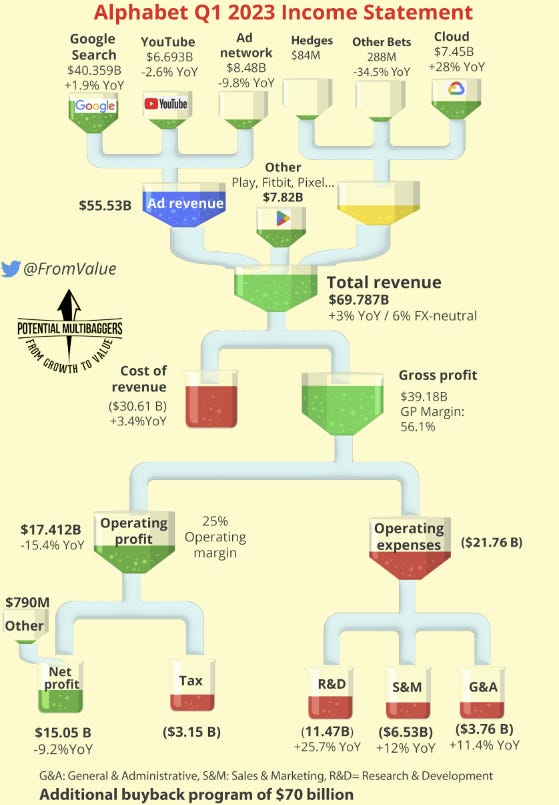

The visualization and a very quick analysis

Hi friends

At Potential Multibaggers, I have earnings deep dives, but here I publish my earnings visualizations and sometimes quick takes. And this is one for Google.

I hope you don’t mind me using the name Google, even though we all know it’s Alphabet. If they want me to use Alphabet, they must change the tickers from GOOG and GOOGL to something else. :-)

Google’s stock is up about 1 % at the moment of writing this in the after-market trading but it was up much more initially. Without further ado, here’s my visualization of the earnings.

A few takeaways

The company beat revenue expectations by a casual $1 billion, $69.8 billion versus the consensus of $68.8 billion. That’s up 3% YoY but would have been 6% on a constant currency basis.

Alphabet (ok, ok, I’ll use it) also beat on EPS: $1.17 versus the expected $1.07. Noticeable was that the Cloud division was profitable for the first time.

Despite 28% YoY revenue growth for its Cloud division, management said they saw longer sales cycles and shorter-term contracts due to the macroeconomic circumstances.

Google, the ad-powered side of Alphabet, keeps struggling with flat or negative numbers. Again, not surprising with the macro headwinds we see everywhere.

Guess what was one of the most-mentioned words on the conference call? You guessed it, AI. It was probably mentioned more than 50 times. CEO Sundar Pichai said Bard was upgraded but also that the company often uses AI behind the screens, for example, for ads.

Overall, margins were down. The operating margin came in at 25% versus 30% last year. But compared to Q4 2022, operating margins are improving, up from 23.9%.

Next to the beat to the top and bottom line, the initial big rise in the stock price could have been caused by the announcement of an additional repurchase program of a whopping $70 billion. That’s just a crazy amount. With that money, Alphabet could buy Airbnb or Target; or even Shopify and Snap together.

Google still has a huge market leader position in search, with a worldwide Search market share of 93.17%. Bing doesn’t seem to have a huge impact for now.

Google trades at a forward PE of 20.9 now and with continued expected EPS growth in the low to high teens, I think the market has some recency bias, thinking that the tighter ad budgets are forever.

Overall, this quarter was not great, but better than expected. As long as the economy is not doing well, ad budgets will be impacted, which will have consequences for Google’s revenue. But I don’t see any fundamental changes that warrant extra scrutiny. I remain a happy GOOGL shareholder.

In the meantime, keep growing!