A Banker Analyzes Nubank

A Banker Analyzes Nubank

A deep analysis of Nubank from an insider working at one of the biggest global banks.

Hi Friends!

Here’s an update on Nu Holdings (NU) that was previously shared on Potential Multibaggers, my paid service on Seeking Alpha. I picked NU at $4.47 in April of 2023 and I have made it a relatively big position in my portfolio since then. This is the kind of deep analysis you get there.

If you want to subscribe to Potential Multibaggers, there’s a two-week free trial and a 20% discount if you decide to stay if you use this link.

If you just want to stay here, don’t forget to subscribe here, so you get these FREE articles.

If you are new to this company or have been a shareholder for a while, I think you will thoroughly enjoy this article. It was not written by me but by Karan, a banking insider, as he works for one of the biggest global banks. Therefore, it’s very interesting to see how a banking specialist looks at this “new bank.” For Potential Multibagger subscribers, Karan gave his insights already several times, but I think that as a subscriber to Multibagger Nuggets, it’s also time to get to know his deep analysis. So, here we go. Karan, the floor is yours.

Hi there!

I’m Karan, and I’ll be guiding you through the wonderous world of Nubank.

Before I start, if you haven’t heard Kris’ conversation with Fede Sandler, this is your reminder to do so because of his original insight and also because his influence can still be seen in the materials both Mercado Libre and NU put out, which is, exceptional.

Just as an example, here is JPM’s earnings, widely considered the gold standard for banking - 1Q24 Earnings Presentation (jpmorganchase.com). Remember to keep this in mind as we go through what NU puts out instead.

I hereby christen NU the new (see what I did there?) The Trade Desk, an absolute firehose of information that takes 90 minutes to listen to and days of editing to deliver the key points. Bear with me if this is on the longer side, but NU puts in a lot of work to educate us about their business, and it’s absolutely worth seeing all the deep insight management provides.

NU laid out its strategy going forward and also provided us yardsticks by which to measure them, neatly captured as follows: (from the conference call)

First, establish strong momentum in Mexico, which means creating the basis for us to grow sustainably and profitably in the country; second, ramp up our secure lending initiatives in Brazil; third, enhance our strategies to further advance in the high-income segment in Brazil; and fourth, launch products and services to leverage technologies such as real-time payments, open banking and AI that will turn the concept of our consumer technology-driven money platform into a reality for our customers.

This quarter shared some information about point 1 which I’m sure you’re eager to learn more about

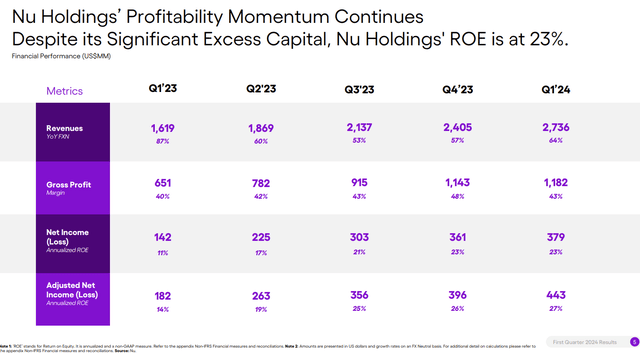

Before we go to deeper insight, let’s first check the numbers.

The Numbers

Q1 2024:

Revenue: BEAT

Revenue of $2.7 billion(+66.7% Y/Y) beats by $170 million. Analyst expectations were $2.53 billion.

EPS: BEAT

Q1 GAAP EPS of $0.08 was in-line.

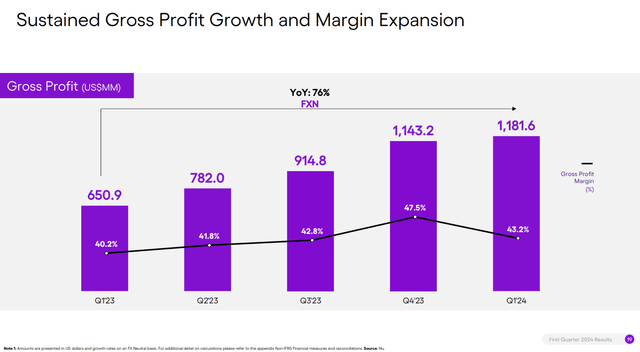

Gross Profit:

$1.18 billion, a 76% increase YoY currency-neutral (FXN from now on). Gross profit margin stood at 43.2%, up from 40.2% in Q1’23

Key Business Metrics:

Purchase volume was $31.1B vs $32.6B in Q4 and $23.3B in Q1 2023

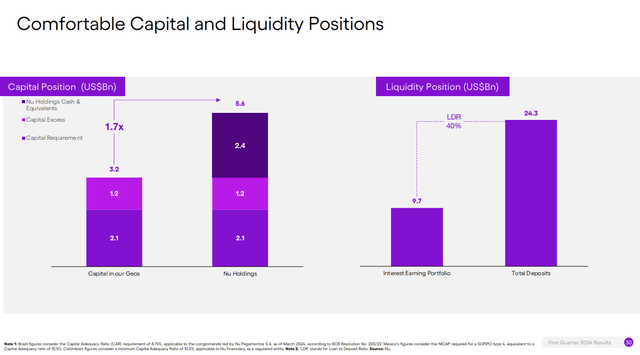

Liquidity:

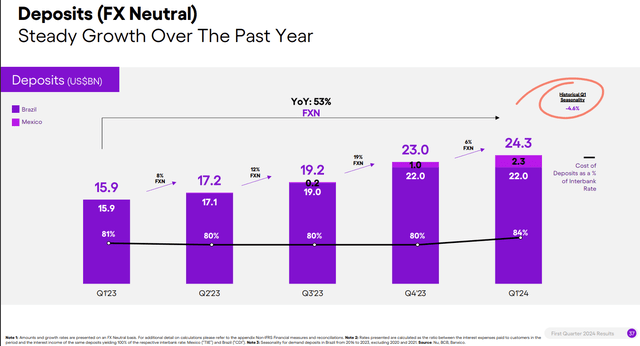

On March 31, 2024, Nu had an interest-earning portfolio (IEP) of $9.7 billion, which rose 86% YoY FXN, due to the ramp-up of personal loans and credit card receivables in the past 12 months. Total deposits increased to $24.3 billion, Nu’s loan-to-deposit ratio reached 40%, versus 34% in the previous quarter.

Gross Margin:

GAAP gross margin in the first quarter of 2024 was 83.5%, an increase of 130 basis points from 82.2% in the first quarter of 2023. Non-GAAP gross margin in the first quarter of 2024 was 84.9%, an increase of 100 basis points from 83.9% in the first quarter of 2023.

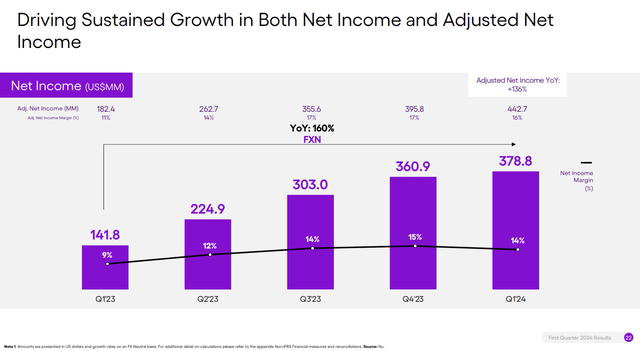

Net Income:

$378.8 million compared to a $141.8 million profit in Q1’23

Adjusted net income of $442.7M rose from $395.8M in the prior quarter and $187.6M in Q1 2023

Summary:

“In the first quarter of the year, Nu Holdings achieved an adjusted net income of $443 million, reflecting an adjusted annualized return on equity of 27%. We believe that this performance surpasses that of most peers in the region, despite maintaining a considerable excess capital of $2.4 billion at the holding level and with two subsidiaries in Mexico and Colombia that are still operating with negative profitability. If one were to look at our operations in Brazil alone, our return on equity remained well above 40%.”

Just outstanding results all around, really.

Guidance:

No updated guidance

Now let’s dive a little deeper into the results

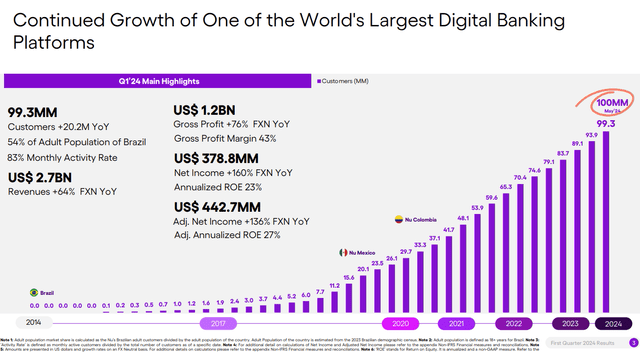

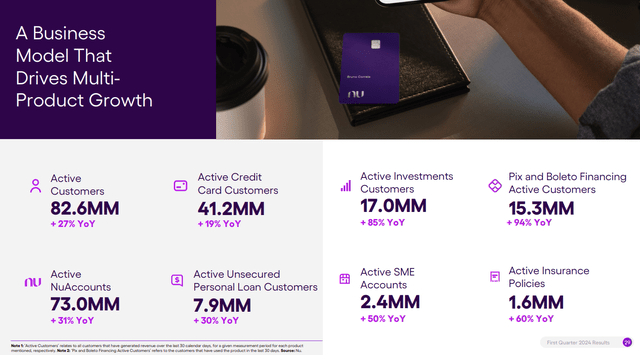

Customers & Deposits

NU is, first and foremost, a rapidly growing bank. We want to check in to make sure that customers and deposits are trending up. This chart alone already gives a ton of information.

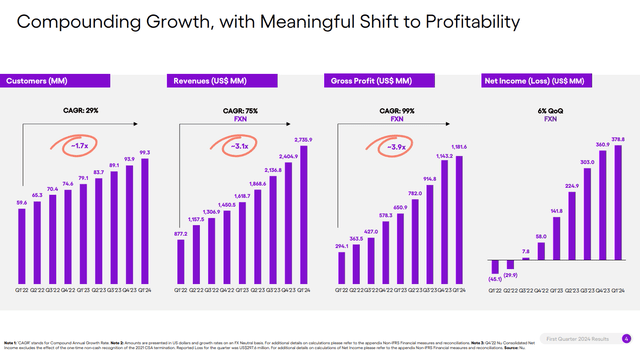

The company added 5.5 million customers in Q1 and 20.2 million year-over-year, reaching a total of 99.3 million customers globally by March 31, 2024. It shortly crossed 100 million customers in Q2 ’24, making it the largest digital bank outside of Asia and the fourth largest financial institution in Latin America by number of customers.

The rate of customer net adds in Brazil averages 1.3 million customers per month, resulting in a total of 91.8 million customers at the end of the first quarter of 2024. This represents more than half (54%) of the Brazilian adults.

But it wasn’t all just a Brazil story –

In parallel, our growth in Mexico has reaccelerated with a net add of almost 1.5 million new customers in the quarter, reaching a total of 6.6 million customers by the end of Q1. This growth underscores the success of our decision to increase the positive yields in Mexico, which has accelerated our flywheel and solidified Nu's position as the unrivalled leader in the digital banking category in Mexico.

We saw updated figures when they crossed 100 million where the split was roughly 1 million in Colombia, 7 million in Mexico and over 92 million in Brazil.

We see steady and consistent growth in deposit balances every quarter, which shows that more and more people are opening and saving with NU.

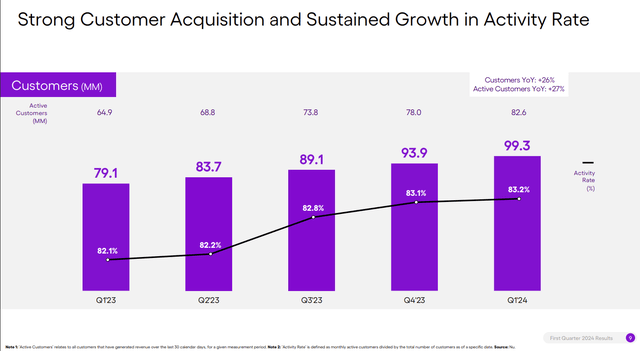

Nu’s product portfolio keeps growing, with credit cards, NuAccounts, and personal loans reaching approximately 41 million, 73 million, and 8 million active customers, respectively. There are currently nearly 2 million active insurance policies, and 17 million investment active customers. This equates to an overall activity rate of 83.2% vs 82.1% last year.

I think it’s safe to say that customers are banking with NU.

Lending

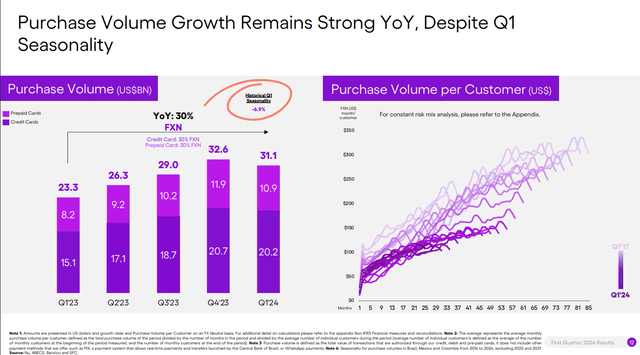

NU is also a ban. Sitting on deposits, doesn’t make money, but lending it out does; let’s see how they’re doing on that front:

A reminder that “purchase” volume is the aggregate amount of all purchases charged to a credit card, not counting revolving balances or cash advances. This is pure “spends” with NU and continues to remain excellent. Q4, of course, covered the Christmas period and is seasonally the strongest, so a dip in Q1 is to be expected, but the fact that it’s up almost 40% vs Q1 last year is phenomenal.

ARPAC translates to Average Revenue Per Active Customer and the fact this is trending higher amongst cohorts basically means more people use more of NU as time passes, telling us the platform is indeed sticky.

As the company said -

In fact, by the end of the first quarter of 2024, we estimate that our market share in cards in general has reached about 15% percent, one five, which would place Nu Bank as the second credit card issuer in the country.

Crazy to think that a startup has achieved this in barely 10 years of operation.

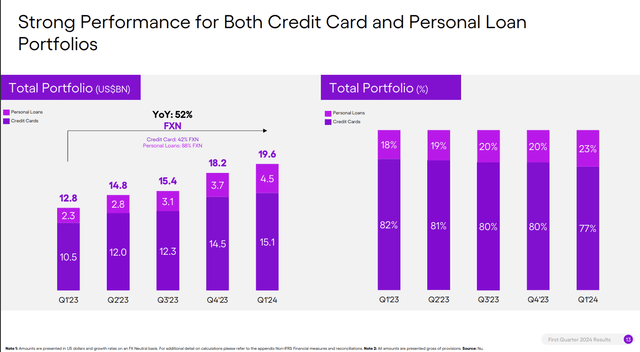

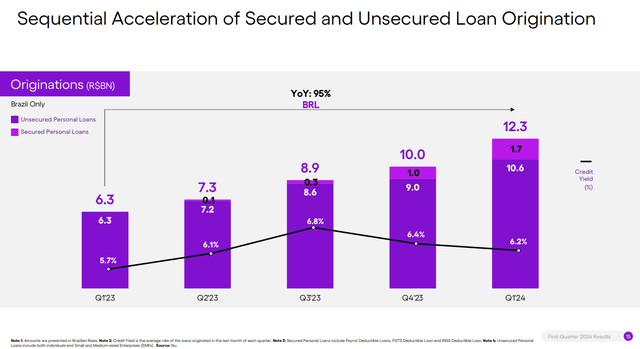

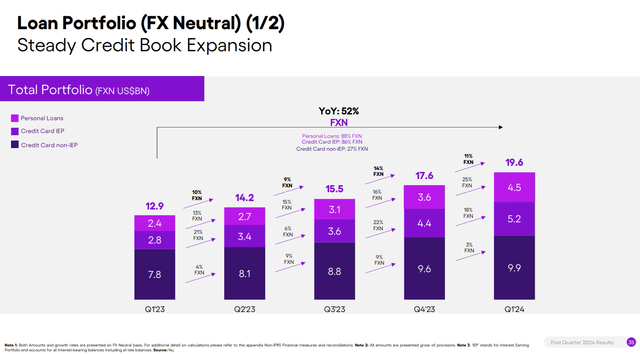

NU isn’t just a one-trick pony. Growth is coming from all segments, which we like to see. Indeed, loans are growing faster than cards, showing us that new product penetration remains healthy.

Secured Personal loans mean loans backed by collateral, whether cash in an account, a fixed deposit, a mortgage, or some other security the bank can claim. Depending on the collateral, this is safer for the bank and can lead to larger loan amounts. Any loan without collateral is, by definition, “Unsecured” and is always the larger category. This is always riskier and, hence, in general, smaller tickets.

Nu Instalments IEP includes -

‘boleto payments’ which allows customers to use their credit card for paying bills in installment;

‘purchase financing’: allows customers to transform existing credit card purchases in installments, directly in the app;

0‘PIX financing’: allows customers to make PIX transactions using their credit card limit and its respective past due balances.

A quick word on this since I promised to cover it earlier, many folks seem to misunderstand how exactly a credit card portfolio makes money, so I’m going to share some details and this will apply as much to NU as it does to American Express or JP Morgan (but NOT to Visa and Mastercard)

There are 3 ways for a credit card portfolio to make money.

When a customer buys something with a credit card, the bank that issued the card will end up with somewhere between 1-2% of the transaction value, depending on the specifics. This will scale with “Purchase volume” above and will happen even if everyone clears their balances in full every month. When you “roll-over” your credit card balance, i.e. pay the minimum due or higher but not the full balance, the bank earns interest on the balance. This is the most commonly thought-of mechanism.

There is a difference between “rollover” and “delinquency, which is that people who pay the minimum due on their statements are deemed to have rolled over and are not “Delinquent”.

As an example, if Kris & I both spend $10,000 dollars on our cards, our statements will show a balance of $10k and a “min due” – of $100 (as an example, most min due is calculated as X% or $Y whichever is higher, I have taken 1% to illustrate)

So, if Kris pays 100 dollars, he has met the min due and he rolls over $9900 to the next statement.

If I only pay 50 or nothing, I am deemed “delinquent,” and $9950 is rolled over to the next statement.

The bank will earn interest as per normal from Kris, on $9900, computed daily and charged monthly. In my case, the bank will earn interest on $9950 but also charge a late fee, which is additional revenue.

It is important to remember that many people pay off their balances in full every month, and the bank earns no interest on these customers. The vast majority of interest revenue is earned on revolvers and delinquent customers.

Credit Card Interest generally compounds; hence, interest starts getting charged not just on the outstanding principal but also on outstanding interest from prior cycles. This is how a “debt snowball” occurs with larger and larger balances over time. But the key is this can only happen when you are multiple installments behind on your payments, and hence “Non-Performing” is typically defined as 90+ days overdue, i.e., you have failed to pay at least the minimum for 4 consecutive months.

As we will see shortly, only 5% of customers become delinquent, and an even smaller proportion of these will pay high default interests in Brazil, as claimed by a recent article. This DOES NOT mean however that 95% of people owe money to NU and rollover their balances, most will pay every month with no problem, while a smaller number will pay higher than min due.

In summary,

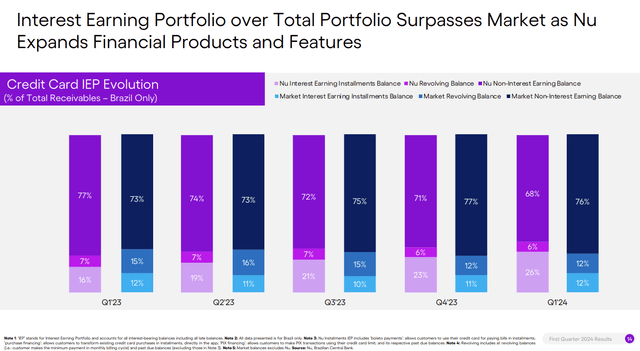

An “IEP” or interest-earning portfolio will include all interest-bearing balances, including late balances. A “non-IEP” will be a balance that doesn’t earn interest, likely because it’s being paid off every month. Once we factor that in, we get this picture:

Once again, we see that NON-IEP balances are the largest and always have been because, as I mentioned, most customers pay off their balances every month. What we see is that the IEP portions are increasing, which is how NU is able to grow revenue, through its innovative products.

Now, you may rightly ask, is this a problem? Is it that NU’s new customers are unable to pay off their balances? Or are people getting stretched and are hence unable to pay?

This is where we must remember that NU’s deposit ratio (loans/deposits) is 40% vs. 100-110% on average in Brazil, so if anything, NU is catching up to the market average, and even this is very prudent. As the company said:

Yes. So, I mean, a good reference more than a guidance is the loan to deposit ratio of the large retail incumbent banks in Latin America, is between 100% to 110%. I don't expect that we will get to a loan to deposit ratio anywhere close to those levels, but it will be materially higher than the 40% that, we presented in the last quarter.

What we are seeing is a maturing credit portfolio where risk and reward are traded off. That said, we need to try to ascertain just how much risk NU is actually taking in growing these balances.

Delinquency

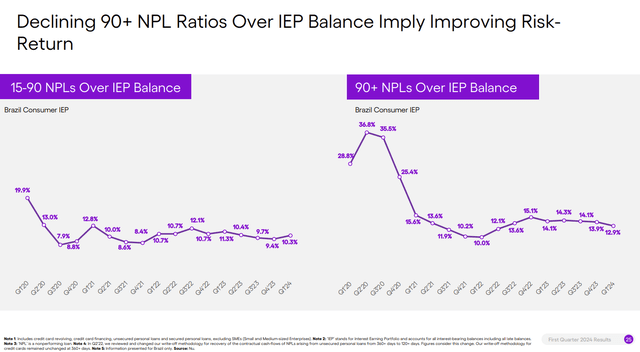

This is where the rubber meets the road. You can theoretically grow your loan book to 1 trillion, but you won’t get most of it back. You have to have strong underwriting and strong Collections to keep this in check. Delinquency is the best way to understand your success as a lender and profitability.

In Brazil, the consumer credit portfolio’s 15-90 NPL ratio was 5.0%, which is in line with expectations and historical seasonality. The 90+ days NPL ratio was 6.3%, also in line with the expected stacking behavior of the early delinquency buckets from previous periods. Part of the growth of NPL has been coming from expansions down the credit spectrum, as the company continues to see meaningful opportunities to expand its credit portfolio, aiming for attractive returns and robust resilience. When excluding credit and looking at interest earnings balances only, Nu’s NPL has been trending significantly down both on 15-90 and 90+.

This is what we want to see. As someone who does this for a living, I can confidently tell you that growing a loan book by 40% with flat NPLs and delinquencies is a momentous achievement. This is as close as possible to the Holy Grail of Credit Cards as an institution.

The Formation Ratio measures the net increase in bad loans by adding back write-offs and sales of soured credit as a proportion of total advances. Long story short, this isn’t climbing as fast the loan book and is quite stable overall, so something to keep an eye on, but not something to really worry about.

For those nervous about this uptick and fearing the worst, I’d also like to paraphrase this exchange from the call to share more about how management thinks about their credit book.

Mario Pierry, analyst:

Hi, guys. Thanks for taking my question. I wanted to stay on asset quality. When we look at your NPLs, they are at the highest level in the series, right? The NPL over 90 days is 6.3%. When I look at your loan, Stage 3 formation at 3.7%, also historical high. You talk about the increase in expected losses on your release, or you had an increase in expected losses because you're increasing the risk profile of the newer cohorts.

So, what we're seeing in Nubank is very different than what we're seeing at the other banks in the system in Brazil, where the banks really became very cautious in lending, and seeing now NPLs improving and asset quality improving.

So I wanted to, pick your brain as how can you be so confident, right, in continuing to take on more risk? Why do you think that the consumer in Brazil is in good shape? You already showed that the interest portion of the credit card is at 26%, well above the industry. And so, the ability of the consumer to continue to take on more credits and more risk, clearly, right, you are pricing that, you're increasing your return on your loans, but eventually gets to a level that is too high. So, you know, just trying to pick your brain here, it seems like you're moving down into a riskier segment of the population, while everyone else is doing the opposite. So that's my question?

Youssef Lahrech, President and COO of NU Holdings:

So, let me maybe address or remind us a little bit about, how we think about credit on writing, if you'll allow me, and then I'll address specifically the latest trends. So when we underwrite credit, our objective is not to minimize NPLs. Rather, our objective is to maximize the NPV of that credit grant to maximize the NPV of that customer relationship, subject to resilience constraints, right? So specifically, we want to ensure that every credit grant that we make is NPV positive, even in the event of a downturn.

NU makes it clear that they are NOT optimizing for low delinquencies, but in fact, for profitability. This runs counter to many mature institutions that don’t grow as fast and, hence, need to play defense in order not to lose too much. But because NU is growing so quickly, they have a higher risk appetite. In simple terms, if they think there is money to be made by lending to a group of borrowers that other banks are shying away from, that is a bet they are willing to make. As they go on to explain

So, we typically don't take a position with respect to timing, the point of the cycle at which we're at. We're fairly agnostic to that. We want every origination we make to performing good and bad times. So when we see opportunities to expand credit and taking a little bit more risk, especially, with products and features that customers love and create a lot of value for them, like we see with some of the financing products we've introduced, like Pix financing on the credit card or unsecured loans.

We're not shy about taking that risk, but we always do it with very rigorous testing, sometimes testing for months and several quarters, before we roll out, and very rigorous monitoring of the risk and return that we get as a result. And we've been very happy with the results of those expansions, as I mentioned earlier, be they in personal loans, secured and unsecured, or in credit cards, as you can see in the expansion of our interesting earning portfolio that Lago talked about.

It’s not that they don’t care about risk, they care about risk vs. reward.

One way perhaps to think about the dynamic - in our credit book, is looking at the data we shared on Page 25 of the earnings presentation, which shows you NPLs as a ratio of interest earning balances. You see there that we've grown interest earning portfolio balances faster than we've grown NPLs. And that's a simple way to kind of validate that this is a creative to return than NPV. So again, this is not a result of us taking a particular position on where we are at the cycle.

It's rather us testing over months and quarters and years, new products, new features, observing the returns, and then deciding to roll out, when we see really good and resilient returns on that.”

&&&

One point I would add just to close on Youssef’s explanation is, the majority of the additional products, financing that we have been launching, that we've been growing are very short time duration in nature. We're talking about 30, 60 days type of loans. So these tend to be a really high information risk type of product that are losses through react very quickly to any signs that we might see, things that are not playing out as we expect.

Again, we're making an underwriting decision based on a view of an NPV model, based on a lot of testing, based on a lot of foundational testing that we're doing. And the ability to do this type of short-term, short duration products just allows to increase the financing portfolio that we have, while maintaining significant control on the risk of the portfolio.

I mean that about explains it, they are willing and able to take on more risk and as a result, willing to tolerate higher delinquencies, because they believe they will make more money than they lose. This is the essence of risk management at its core.

Analyst of the day, Mario Pierry, then followed up with another great question.

Okay. Let me ask a follow-up here. When I look at your credit cards outstanding in Brazil, it went up by about 200,000 from R$37.5 million to R$37.7 million, even though your active clients in Brazil grew by 3.6 million. So this is the slowest pace in the increase of number of cards, right? The average, you're growing about 1.8 million credit cards in Brazil in 2023, per quarter. Now you did 200,000. What does this mean? Does it mean like you are being more conservative, or you reached a percentage of your client base that they don't have the capacity to take on a new credit card?

Again, we should applaud the analyst for a great question – how can you tell me that you’re confidently taking risks and growing the loan book if your credit cards aren’t growing that fast? Aren’t you just exposed to existing customers taking on more risk?

NU had an equally good answer:

Mario, one thing that I would point out, and I'm certainly let my other colleagues chime in, is that in Brazil, as we start to approach 55%, 60%, 65% of the adult population, it's inevitable that the marginal growth will not necessarily come from adding more customers or more credit cards to the existing customer base. We still have a lot to go there, but it's only natural that at some point in time, the growth in number of customers of the number of cards will diminish.

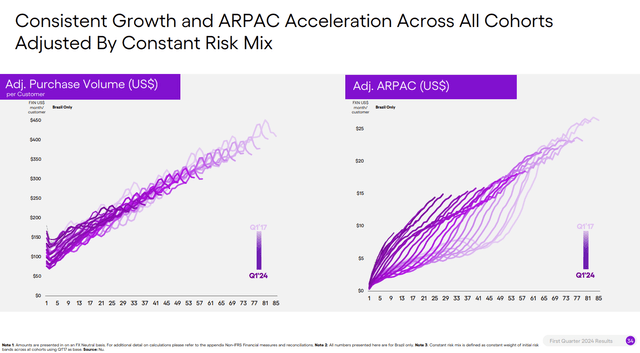

But what we still have plenty of room ahead is what you can see on Page 34 of the earnings presentation. And you can see the evolution of the purchase volume and evolution of ARPAC as the customers mature. So even at the customers that we have on board 24 months ago, they are tripling their purchase volume as they mature their usage with us.

So what we will naturally see in Brazil is that a natural kind of a flattening of the curve of number of customers and credit card customers, but the continuous evolution of the maturation of purchase volumes in ARPAC. And then conversely, Mexico and Colombia are in the very early days of the expansion of number of customers and number of cards. So, they are in a different point of the S curve cycle there.

Yep, that makes sense to me, after all NU is now the second-largest credit card issuer in Brazil already, so we should expect to see new customer growth for cards slow down, while existing usage increases and that’s exactly what we’re seeing.

Another important note here is that while the percentage of delinquencies is relatively stable, the absolute dollar amount increases because the portfolio is simply much bigger. And this means greater loan loss reserves and coverage ratios, which bears out:

Coverage ratios are trending higher, as they should, given NPLs in terms of dollars are higher, as they should, the main thing here is that there is a healthy cushion.

There was an excellent question on borrowers renegotiating their loans, known as “restructuring.” Here is what NU said about renegotiation:

So renegotiations loans still account for about 10% of our portfolio. It has not changed materially since we last presented this. We do expect that we will be disclosing our renegotiation rates, on an annual basis at the - whenever we disclose our fourth quarter results. In addition to that, you can see some levels of renegotiations in the filings that we present to the local regulators, especially in Brazil, that we do on a six-month basis.

All in all, I’m not worried at this stage, but it is curious to see if they will become more conservative as Brazil matures and we see a shift in tone in the future.

Summary of Performance

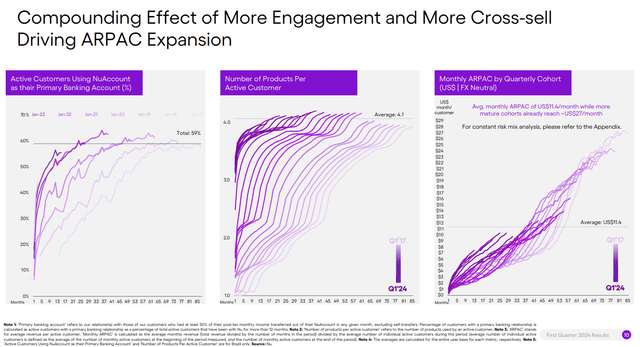

The monthly average revenue per active customer of $11.4 rose from $10.6 in Q4 2023 and $8.6 in Q1 2023. The monthly average cost to serve per active customer held mostly stable at $0.9. More mature cohorts have an ARPAC of $27.

For those counting, it costs them 90 cents to serve a client while they make $11 of revenue from them (up to $27 for the more mature users). This is completely crazy when compared to developed economies, as banking is generally a low-margin industry, but it just shows you the power of an oligopoly in an emerging market.

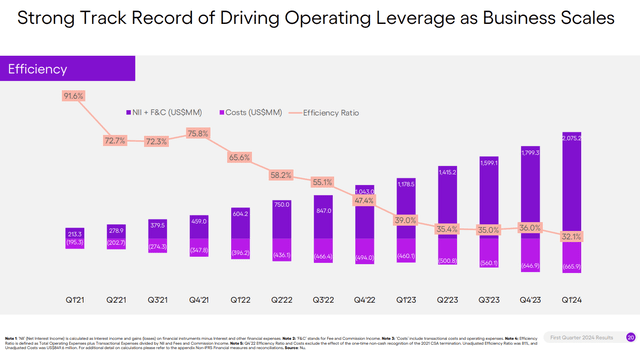

I was taught that growing revenues faster than expenses is called Operating Leverage and NU definitely calls that out.

The company’s efficiency ratio stood at 32.1% in Q1’24, which strengthens Nu’s position as one of the most efficient companies in Latin America.

In comparison, the best banks in the world (as an example the top 20 US banks) average efficiency ratio at 53%, with JPM being best in class at 51%. Source: US banks' efficiency ratio hits 10-year low as noninterest income spikes | S&P Global Market Intelligence (spglobal.com).

To be honest, I didn’t have time to update the figures but given JPM guided to higher expenses this year, Guru Focus tells me that has increased to 54%. Source: JPM (JPMorgan Chase) Efficiency Overhead Ratio % (gurufocus.com)

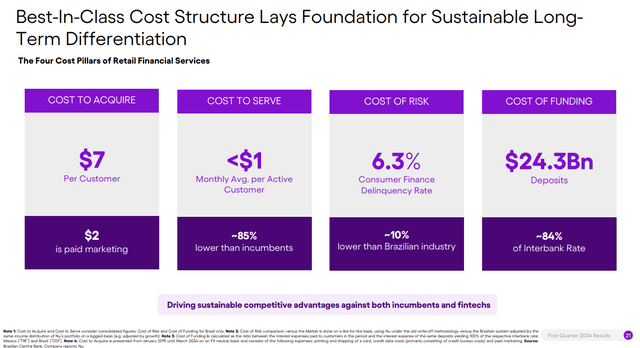

So, NU is enjoying the benefits of being “New” with a best-in-class technology platform and no legacy costs or technical debt. This gives them such an enormous advantage over incumbents in LATAM.

The joys of a modern banking platform. I know a few financial institutions that would kill for a single-digit CAC.

And in conjunction with this, we saw that S&P Global upgraded Nu’s credit to BB globally and brAAA in Brazil. (Source: Nu Financeira S.A. Upgraded To 'BB' And 'brAAA' O | S&P Global Ratings (spglobal.com))

In Summary, this gets us

We see this across cohorts old and new:

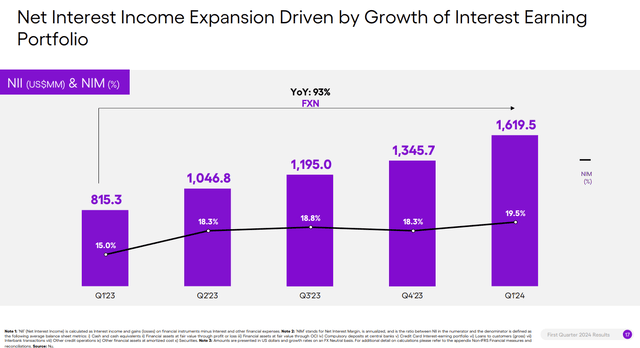

Net Interest Margins are growing at a healthy clip, primarily driven by the increase in lending.

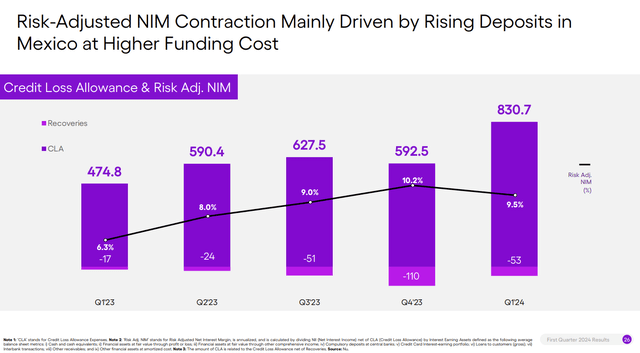

That said “Risk-Adjusted Net Interest Margins” saw a minor decline this quarter after 4 straight quarters of growth. The culprit? Mexico, where the company decided to offer higher rates to attract borrowers. We will discuss Mexico a bit more later on.

Going back to basics, revenues are up, costs remain low, and profitability should be up, and it is.

That’s a beautiful chart.

Case Study: Mexico

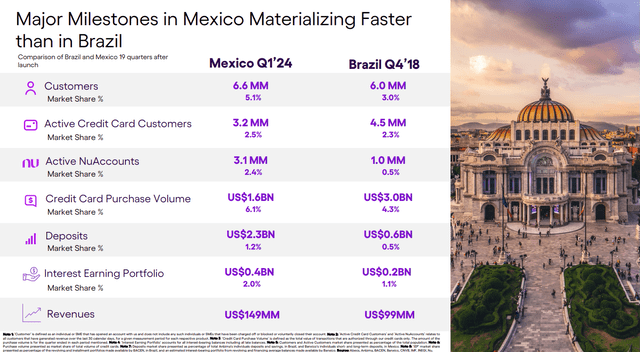

As I mentioned at the beginning, NU provided some details on Mexico as their next growth engine. Nineteen quarters after launch, Mexico is already surpassing Brazil in terms of time to achieve different key KPIs.

In just one year since the launch of Cuenta Nu, Mexico has surpassed Brazil in absolute account holders and penetration of the total population compared to the same time of the Brazilian operation. Deposits in Mexico have also soared to surpass $2.3 billion in Q1’24. In the credit card space, Nu has over 3.2 million active credit card customers, outpacing some of the top three incumbent banks in the country.

These are incredible numbers and led to one of my favorite slides in the presentation:

I wish more companies would do this. NU is basically comparing Q1’24 in Mexico to Q4’18 in Brazil when they were at a similar stage of growth. This shows us that the company is making more progress, much quicker than it did in its home market. NU’s financials will look phenomenal in about five years if this continues.

The company specifically called this growth out as well, I am pasting the entire commentary in full because it’s very educational and informs the thesis for both NU & MELI, which applied for a banking license.

David Velez, founder and CEO of Nu Holdings:

Hi, Eduardo. Here's David. So listen, Mexico is a really attractive market for a number of different reasons. One of the interesting reasons that, has become much more visible to us recently is that differently from Brazil, the deposits as a product is the largest source of profit for the incumbent banks. So when you look at the average yield that banks are paying consumers, it's something like 3% to 4% a year when you have an interest rate, a sovereign interest rate in the 12%, 13% plus.

So this is a bit of a normality in a regular banking market, because banks are effectively making significant profits without really taking any risk. When you look at Brazil, you see a market where that is driven very much by taking credit risk, which generally is what you would expect in competitive markets. That's not the case in Mexico. And when you look at the level of interest rates in products, they are still very high. So in a product, when we make or unit - we look at our unit economics, even at offering a very high yield, we're still making positive unit economics given the structure of the market.

Now, given the fact of how these profits exist in the system, we think there's a really interesting disruption opportunity for the entire Mexican system, because if most of your profits are coming from deposits, frankly, the barrier to entry is not that high. Yes, probably in the past you needed branches. Now you don't. And yes, brand is important, because consumers won't leave their life savings in a brand that they don't trust. But the reality is, if you have a good brand and you have a very good product, you will take those deposits away.

And I think the past six to nine months and the pace of growth that we're showing with this yield is showing very significant growth, above our expectations and much higher than fintechs that are paying even higher yields than we are. So, we're not only necessarily just competing by higher yields. You are already being able to see that we've built a very solid and trusted brand in Mexico. And this is being a big source of deposits. Now, all being said, I think in the long-term, we will also rationalize the cost that we are expecting. We tend to make this decision based on value proposition.

Our goal, is to have the very best deposit value proposition in the country. That is a function of yield and features. Initially, our features were not that big, which meant we had to rely a lot on yield. And that's what we're doing right now. But very soon our features have been growing and by the end of the year will be a very different product. And you mentioned cash in cash out. That was a significant bottleneck that we had a few months ago. We are solving that as we speak.

So as we increase the level of features, as we increase the value proposition, as we strengthen the brand, we expect to be able to decrease yield while maintaining the best value proposition. We think that incumbent banks, are going to have to increase the yield that they offer in consumers, if they want to keep a lot of these consumers. Ultimately, in this new world, there's just not that many buyers of entry, and you just cannot keep your consumers trapped. They will go to whoever gives them the best option. And so, we think we are on path to building that product in that category that way.

Guilherme Lago

Rosman, if I may add one thing, what we have been seeing in Mexico, as we have seen in Brazil in the past, is that as we attract deposits from customers in the country, we are also benefiting from very relevant second order impacts. That allows us to increase our brand awareness. It allows us to increase credit card applications. So credit card applications have more than doubled in Mexico since we repriced our deposit products.

It allows us to acquire data, to do better credit underwriting and customer segmentation. It gives us positive credit selection. So there is a tremendous amount of second order impact that, the deposit flows are bringing to our flywheel that, are not necessarily capture only in the absolute nominal amounts of deposits that we see coming in.

I look forward to hearing more about the growth story in Mexico.

Untapped Growth Opportunities: SME Business

We saw incredible progress on both Cards and Personal loans, but there is a huge driver slowly growing that hasn’t gotten much attention yet, which is the small and medium business market in Brazil and Mexico. Once again, I refer to a part of the conference call which was very educational:

“I have a question about the SME business of Nu. We saw that Nu already achieved more than 4 million clients in the SME business, something close to 2.4 active clients in this segment. When you look to central bank data, Nu is charging about 9%, 10% per month in these short-term work capital loans.”

NU’s response:

Thank you for the question. So you're right, we actually haven't really talked publicly that much about our growth on the SME side, but it is a significant opportunity ahead of us. And partly this opportunity has come to fruition, as we started to cross-selling SME account to our large consumer base. So just to give you one data point, out of the 93 million or so Brazilian customers that we have, we think we have in our base something like eight or nine million small businesses.

And that's a significant percentage of something like 15 million of total businesses existing in Brazil. So already in our base, we have a path towards pretty significant operation with small businesses. We, by the way, see that they tend to be very badly served also, especially if they are owned by one shareholder or two shareholder.

So this is a big opportunity that we've been developing, as it has grown consistently. Today, our value proposition is fairly basic. We began with an account for the small business, then we launched a debit card. We have already started growing for a few quarters the credit card for the small business. This is a product that we're very excited about, because we get to use a lot of the credit and the rating data that, we have on the consumer side for the small business side.

There actually is a lot of synergies, in using a lot of the data for both sides of the consumer, and allows us to see a consumer more, with a more complete basis. And we also see that, when we start banking somebody both on the consumer side, as well as the small business, we see a pretty significant increase in ARPAC. We see a higher increase in engagement. We see higher activation. So, it not only adds additional ARPAC, it brings a lot of synergies to the platform as a whole.

In terms of working capital loans, we are just beginning to test that product. It's tiny in our base. It's something that we are ramping up slowly. And we're testing a number of different secured and unsecured products for the small business, but we haven't really rolled out anything big yet.

And within credit, we started with credit card for SMEs. The credit card business, is performing extremely well. We are super encouraged by the early results, and then, we are now gradually expanding into working capital.

In summary, NU already has relationships with about half of SMEs in Brazil due to its consumer business. If it is able to cross-sell and expand with more products like working capital loans, we see the germs of an institutional business being built that hasn’t even been factored into the company’s growth trajectory yet. It can be a risky segment, but with a different economic profile from that of a small borrower, every large bank is always more profitable on the institutional side than the consumer side. Watch this space with excitement because I certainly am!

Note on Telecom

After the earnings call, we also heard that Nu is entering the Brazilian telecom market. It recently secured Mobile Virtual Network Operator (‘MVNO’) approval through a Claro partnership, paving the way for a third-quarter debut.

I was very confused when I heard this because I am neck-deep in delinquencies and unsecured loans. But step back for a moment. NU is ultimately a technology platform, not a large bank with 10,000 branches. What is the impediment to its growth? Internet Access. The more people with internet-enabled smartphones, the more they can access services and transact via NU.

This is no different from what they do with insurance and other non-core products, where they partner with companies that do the heavy lifting in terms of assets while NU cross-sells to its existing base. In his talk with Kris, Fede Sandler also pointed out that, while everyone knows the company as Nubank, they went to the stock market as Nu Holdings, which already implied they could add other technologies besides just banking.

Here specifically, instead of buying data from major telcos and charging a margin like other MVNOs there do, Nu is creating a revenue-sharing agreement with Claro. So, Claro does the heavy lifting at the back end, NU brings the customers, sounds like a win-win to me.

Stock-Based Compensation

Unlike most companies, FCF doesn’t really work for banks because the Cash Flow statements are all messed up. Instead, we look at absolute SBC, which was significantly higher this time around at almost 79 million USD (source: Finchat). This prompted a question on the call from an analyst who was thankfully paying attention:

“Share based compensation was quite a bit higher this quarter than it has been. Can you just remind us of the dynamics? There is the share price, a driver, is it about grants? What's going on? What drives that? And how should we think about a normalized level?”

NU responded with:

Yes, we had an increase in share-based compensation. And I think, it is largely the result of three compounding effects. I think number one, is there's a general headcount growth in the company. Number two, is the result of no more aggressive performance recognition that we did in the first quarter of 2024, compared to the first quarter of 2023.

And number three, the share appreciation, which negatively impacts our social tax contributions, primarily in Brazil, which can account for up to 36% of the grants. So as you will see in our explanatory notes for the financial statements, you will note the increase in share-based compensation, but also the corresponding increase in share taxes and social contribution taxes, which are accounted together with share-based compensation.

Ok, so both the headcount the stock price went up and so did the costs and taxes as per rules and regulations in Brazil. Is this something we will just have to live with forever?

Now, one of the things, Geoff that we take, very seriously is the net and gross dilution that we apply to our shareholders. And if you take a look at our gross and net burn rates, we have been operating below 100 basis points. In fact, over the past two years, we have been operating below 60 basis points. And we believe the number one that we are in the bottom quartile of the industry, in terms of companies that apply the lowest levels of dilution, to our shareholders.

And number two, as we increase in size and value, we do expect operating leverage to continue to play its part here. So, we expect that this number will actually go down over time.

I can live with 0.6% dilution for a company growing earnings by triple digits, especially if the SBC will rather fall than rise.

Balance Sheet

In a word, it is extremely healthy, and NU remains conservatively managed.

Summary

This was an exceptional report from NU and a personal boost to my conviction The company is firing on all cylinders, growing profitably and being realistic about the risks of doing so Mexico is in its early stages and yet promising, SME business is in even more early stages and full of potential Great quarter guys, this slide basically captures it all, long may it continue!

This translated into a 75% annual compounded growth rate for this period. Wow. Just wow. Crazy Wow.

If you like this deep analysis and you want more, there is more at Potential Multibaggers, MUCH more (over 1,000 articles!). You can try it out for free for two weeks and you get a 20% discount if you use this link.

Of course, you can also just subscribe to Multibagger Nuggets and get these posts for FREE.

If you find this valuable, don’t be shy about sharing it with your friends!

In the meantime, keep growing!

Loved your takes from experience in the field.

Great job Kris!

I included a link to your post along with links to some other recent write-ups about Nubank in last week's links post: https://emergingmarketskeptic.substack.com/p/emerging-markets-week-july-8-2024